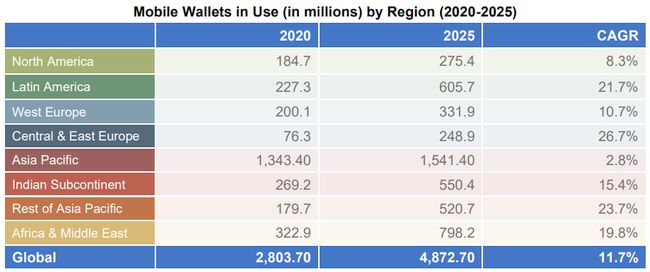

The biggest report ever on the growth of mobile wallets projects that one in two people will use a mobile wallet by 2025. At the end of 2020, there were over 2.8 billion mobile wallets in use. That number is projected to increase by nearly 74% to reach 4.8 billion mobile wallets in use by the end of 2025 – nearly 60% of the world’s population. The fastest-growing markets are Southeast Asia, Latin America, and Africa & Middle East where mobile wallets are displacing cash and cards for more convenient digital payments.

Boku, a fintech pioneering the world’s first global mobile payments network, has released its 2021 Mobile Wallets Report in partnership with digital technology analyst house Juniper Research, which provides insight into mobile wallet adoption and use in leading markets across the globe. In 2019, mobile wallets overtook credit cards to become the most widely used payment type globally and the shift to online driven by the pandemic has accelerated adoption. Mobile wallets use is growing rapidly across the world with emerging markets leading the way.

Key findings

– Southeast Asia is the fastest-growing mobile wallet region

Mobile wallet use will grow by 311% between 2020-2025, reaching up 439.7 million wallets in use across Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam from 141.1 million in 2020. The rise in e-Commerce and the dominance of super-apps like Grab and Gojek, particularly in markets like the Philippines and Indonesia, is driving accelerated mobile wallet adoption.

– China reaches maturity but Japan, Korea and Taiwan set for hyper-growth

The Far East and China continue to be the largest mobile wallet region in the world with 1.34bn users in 2020. Market saturation is resulting in slowing growth in China with a CAGR of just 2.2% per year. Meanwhile, markets including Japan, Korea and Taiwan will continue to see accelerated adoption of mobile wallets with 98.4% market penetration by 2025.

– Africa & Middle East is the second biggest mobile wallet market

The second-biggest mobile wallet market is set to grow by 147% between 2020-2025. This is driven by expanded usage of mobile money services such as M-Pesa which are increasingly offering additional services such as access to eCommerce.

– Latin American growth is being supercharged by eCommerce

This region is set to increase mobile wallet use by 166% between 2020-2025. Long-held back by consumers’ preference for cash-based payments and comparatively lower smartphone penetration, this is fast-changing, and the region’s eCommerce growth is supercharging mobile wallet use.

– Slow growth in Western Europe and North America

With 65% growth in Western Europe and 50% in North America by 2025, these regions will see the least amount of mobile wallet growth in the next five years. However, markets such as the UK are seeing a rise in card-based mobile wallets due to the adoption of contactless spurred on by the pandemic and shift towards cashlessness.

“While mobile wallets are being used on a global basis, we see two distinct types being used today. One is card-based mobile wallets, like Apple Pay and Google Pay, which provide an easier way to pay with cards people already have. The other is stored value mobile wallets, like AliPay and GrabPay, that enable consumers to transact with digital cash and are popular in emerging markets with fast-growing e-Commerce sectors,” said Adam Lee, Chief Product Officer at Boku. “The markets that are set to grow the fastest are those with the lowest levels of card penetration, stored value wallets are thriving. In North America and Western Europe, which are dominated by card-based mobile wallets, we are seeing the slowest growth in mobile wallet adoption, as the technology provides merely incremental benefit.”

“We are seeing a clear bifurcation in the market between card-based mobile wallets in developed markets and stored value mobile wallets that are ubiquitous in Asia and rapidly growing in all emerging markets,” concluded Lee.

“Southeast Asia is one of the most rapidly digitalizing regions in the world. In 2020, the region added 400 million new internet users, with 70% of the region now online. Together with consumption trends brought about due to lockdowns during the pandemic, that has led to a familiarity with e-Commerce and an exponential rise in mobile wallet use,” said Loke Hwee Wong, Vice President and General Manager, APAC at Boku. “This is also because the region was heavily dependent on cash and bank transfer before mobile wallet use, and the convenience and accessibility, especially with stored value mobile wallets, will see Southeast Asia leapfrog the rest of the world in mobile payment adoption.”

The growth and bifurcation of mobile wallet use present both an opportunity and challenge for merchants. The number of mobile wallets transacting over $1 billion per year is set to grow by 27% from 54 wallets in 2020 to 69 wallets by 2025. This provides a lucrative opportunity for merchants looking to acquire valuable customers, many of whom only use mobile wallets. However, not only are consumers using mobile wallets more, they are using more mobile wallets. Consumers in high-growth markets such as India and Indonesia use an average of 2.74 wallets. This means that not only do merchants need to accept wallets but they need to ensure broad coverage across each target market.

“We are witnessing a paradigm shift in payments driven by mobile wallets. Mobile wallets have lowered the barrier to making digital payments and in parallel ushered billions of new consumers into eCommerce. These consumers are not in North America or Western Europe, they are in emerging markets, and while they don’t have credit cards, they overwhelmingly have mobile wallets,” said Jon Prideaux, CEO at Boku. “For global merchants, mobile payment acceptance is not about accepting one type of mobile wallet or another, but ensuring that consumers in every market will have the required selection on payment types in order to monetize transactions.”

To download the 2021 Mobile Wallets Report please visit our website.

About Boku

Boku Inc. (AIM: BOKU) is a fintech pioneering the world’s first global, mobile payments network. With 45% of global consumers using mobile payment methods to buy goods online, compared to 18% using credit cards, the future of commerce is mobile-first. Boku’s technology platform helps the world’s most demanding merchants attract, convert, and retain customers using mobile payments. By turning payments infrastructure into a source of sustainable competitive advantage, Boku safely activates a range of new merchant business models – from bundling to subscriptions.

Boku’s platform is used in over 70 countries with more than a billion verified transactions in 2020, contributing $8.5 billion to the digital economy. Customers that trust Boku to simplify sign-up, acquire new paying users and prevent fraud include global leaders such as Apple, DAZN, Facebook, Google, Microsoft, Netflix, PayPal, Sony, Spotify and Tencent.

Boku Inc. was incorporated in 2008 and is headquartered in London, UK, with offices in Brazil, China, Estonia, France, Germany, India, Indonesia, Japan, Singapore, Spain, Taiwan, Vietnam, and the US. To learn more about Boku please visit our website.

About Juniper Research

Juniper Research provides research and analytical services to the global hi-tech communications sector, providing consultancy, analyst reports and industry commentary.

Inquiries:

PRecious Communications for Boku, Inc.

Singapore/Asia Pacific: Clarence Lim, boku@preciouscomms.com

Boku in Asia

In Asia, Boku’s payment partners for Mobile Wallets include: AliPay, Dana, GCash, GoPay, GrabPay, KakaoPay, LINE Pay, Ovo, PayMaya, PayPay, Toss, Touch ‘n Go, Truemoney.

Boku also partners with payment partners to offer Direct Carrier Billing: AIS, BSNL, Celcom, Digi, dtac, Globe, Indosat Ooredoo, Jio, Korea Telecom, KDDI, LG U+, Maxis, M1, NTT Docomo, StarHub, Singtel, Softbank, SK Telecom, Smart, Smartfren, Tata Docomo, Telkomsel, Three, TrueMove, Vodafone, XL (amongst others).

Additional insights from the Mobile Payments Report 2021

Other insights from the Southeast Asian region include:

1. Indonesia represents one of the greatest opportunities for merchants accepting mobile payments: its mobile wallet penetration is at 25.6% in 2020, and set to triple to 76.5% by 2025. The report also expects that mobile wallet transactions will increase by volume to 16 billion transactions in 2025 (from 1.7 billion in 2020), and $107 billion in 2025 (from $28 billion in 2020) – the highest in the region.

2. Malaysia mobile payment adoption is behind other Southeast Asian countries currently, at a 31.7% penetration rate, but is poised for hyper-growth over the next five years to 93.9%.

3. Philippines has one of the lowest levels of mobile wallet penetration at 22.4% of the population, but expected to grow to 63.4% by 2025 with a mobile wallet transaction value of $63.4 billion by 2025 (from $15 billion in 2020).

4. Singapore is set to reach mobile wallet penetration of nearly 95% by 2025 from 30.4% in 2020 – the highest in the Southeast Asian region, and with mobile wallet transactions projected to increase by 11x (from 101 million transaction volume in 2020, to 1.1 billion in 2025).

5. Mobile wallet penetration in Thailand is at 21.4% in 2020 and set to grow to 63.4% in 2025. The country is also set to hit $36.7 billion in transaction value in 2020 (from $10.6 billion in 2020).

6. Vietnam is primed for massive mobile payments growth – with mobile wallet transaction growth of 7x expected to 5 billion by 2025 from 674 million in 2020, and a mobile wallet penetration rate of 55.5% in 2025 (from 19.7% in 2020).

As part of the Mobile Payments Report 2021, Boku also conducted an in-depth consumer survey of 1035 respondents in Indonesia, during May 2021, which showed that:

1. Consumers use an average of 3.2 wallets in use per respondent, one of the highest in the world after India. The top reason for using more than one type of mobile wallet included different wallets giving different benefits (63%).

2. Cash was the payment type that is most in use prior to mobile wallets (at 66%), followed by bank transfers (63%) and debit cards (44%), which can likely be attributed to the extremely low credit card penetration rate in Indonesia.