1. Targeted by a short seller, China Medical System fought back with a strong response and large-scale buyback

In recent years it has been common for short sellers who are active in the Hong Kong stock market to target “high-performing stocks”. However, most of these actions have been in vain, the targeted companies with solid fundamentals have withstood these tests and their stock prices performed well again in the secondary market, fighting back against the short sellers.

Recently, the short-seller Blue Orca issued a short selling report of China Medical System, a domestic high-quality pharmaceutical company. In this report releasing in early February, Blue Orca accused China Medical System of inflating profits and its chairman’s misusing of the listed company’s profits for his personal gain.

China Medical System quickly issued a strong response responding to each of the key points in Blue Orca’s allegations. The response also stressed that these allegations were groundless, seriously misleading with untruthful conclusions. Then Blue Orca released a second report which is similar to the first one on February 10. In response, China Medical System further denied all the allegations made in both reports, and claimed that all the allegations were false due to the ignorance of the company’s business structure, applicable tax policies and regulations, and audit process and these allegations are based on incomplete information that was inconsistent with the facts.

Despite the round of confrontation, the share price of China Medical System has not been frustrated, presenting a stable trend and rebounding in the following days. It is worth mentioning that after the short sale, China Medical System bought back 9.648 million of its shares at the cost of HK$ 98.1641 million on February 11. This action not only shows the strong confidence that China Medical System has in its future development but also showcased the company’s sincerity to its minority shareholders and determination of defending against short selling. The company’s shares continue to be in popular demand since the short sale on February 6, with a cumulative increase of 9.8% as of February 14. The response in the capital market clearly demonstrates the failure of Blue Orca’s long planned short sale.

2. China Medical System gives strong response to the allegations. Why the company is so confident?

As a Chinese idiom goes, “If you stand straight, do not fear a crooked shadow,” when facing Blue Orca’s attack, China Medical System not only strongly responded to various allegations in announcement, but also asserted its confidence through a large-scale buyback. The following is a discussion of key views of the confrontation and an analysis of why the Blue Orca’s short selling is untenable.

First, Blue Orca questioned the performance of China Medical System, claiming that the net profit margin of the company’s Chinese branches was significantly lower than the group, and further claiming that the profits from its Malaysian subsidiary were fictitious. In response, China Medical System pointed out that its Malaysian subsidiary, with independent rented offices and employees, undertakes the main international business functions of the company, including new product investment and introduction, manufacturer selection and evaluation, quality control and supply chain management, promotion strategy formulation, etc., and by the end of 2018, its accumulated intangible asset expenditure had reached RMB 2.85 billion.

In fact, given that only a few listed pharmaceutical companies are involved in large-scale international trade, it is not fair to simply compare the business data of China Medical System with other pharmaceutical companies and thoughtlessly conclude that China Medical System exhibited business performance of fraud. Furthermore, from the perspective of China Medical System’s business system, the involved transnational businesses and corresponding structures, established with the assistance of professional tax consultants, are designed to undertake different functions and risks domestically and abroad, then generated corresponding profits, which is a normal business activity and common practice in multinational enterprises. Therefore, the profits of its Malaysian subsidiary really exist, and the profits of the Chinese branches do not represent the overall profit level of China Medical System as a whole.

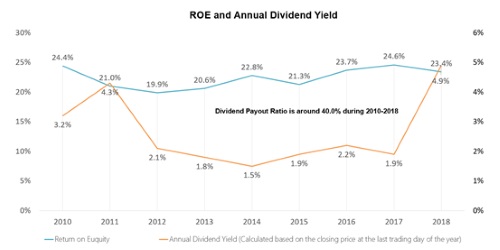

In fact, the past financial performance and dividend payout further authenticate China Medical System’s operation. Since listed in Hong Kong, China Medical System has maintained 40% of net operating profit as its dividend payout for nine consecutive years, totaling RMB 3.95 billion. Publicly disclosed total projects investment is about RMB 4.7 billion. Before 2016, the year-end bank loan balance of China Medical System totaled about RMB 300-400 million; from 2016 to 2018, the year-end bank loan balance of the company was about RMB 1.6 billion, RMB 2.1 billion and RMB 1.4 billion and with a gearing ratio of 16.5%, 20.7% and 13.9% respectively. The gearing ratio of the company has remained at a relatively low level for a long time. Since listed in Hong Kong, the direct equity financing of China Medical System totaled only about HK$ 1.7 billion. If, according to Blue Orca, 49% of the company’s profit was fictitious, then the cash flow would have made it difficult to maintain its normal investments, operations and dividend payout. The company would have been stuck in the mud of cash flow fracture. In light of this, the seemingly exaggerated data argument of Blue Orca is obviously not reliable. At the same time, the long-term performance of China Medical System has obviously registered a soaring growth. Ten years period from 2009 to 2018, the CAGR of its revenue, excluding the effects of the two-invoice system, reached 28.1% and the CAGR of its profits reached 32.9%. Since its listing, the company has been audited by Deloitte, an internationally renowned accounting firm, and its market value has more than tripled.

Second, the other allegation made by Blue Orca mainly claimed that China Medical System, as a listed company, secretly funded the R&D of its chairman’s private company as well as transferred benefits for its chairman’s investment activities.

The root cause of Blue Orca’s allegation lay in its lack of in-depth understanding of the company. In 2015, due to the uncertainty of the policy environment and the expectation of new product launching, Mr. Lam Kong, Chairman of China Medical System, made equity investments. After the successful commercialization of the product in which Mr. Lam Kong invested, China Medical System would then intervene and give Mr. Lam Kong a reasonable return. These were reasonable business decisions and protected the interests of shareholders. After the policy became clear and the team accumulated investment experience, China Medical System gradually explored the model of joint investment by both the listed company and the chairman, and, in some cases, independent investment by the listed company alone. It is in fact a meticulous design made by the company’s founder. On the one hand, as a former medical practitioner, Mr. Lam Kong strives to bring an increasing number of highly innovative, affordable pharmaceutical products which can meet unmet clinical needs of the Chinese market to patients. On the other hand, as a businessman, he has to balance the risks to ensure the company’s future operation and protect the interests of shareholders. Therefore, he chose to invest in the new products projects together with the listed company at the same price and in the same proportion. In this way, the investment risk of the listed company can be shared with Mr. Lam, while the listed company acquires rights of the target company’s products in addition, so as to realize win-win outcomes among the listed company, its major shareholders, minor shareholders and the management. Thus, China Medical System’s detailed response on each project demonstrates that the Blue Orca made false allegations regarding specific project details.

In conclusion, China Medical System counterattacked the short seller by its strength. Notably, this short selling attack by Blue Orca was not only unscrupulous due to the current epidemic and the weakening risk preference in the capital market, but was also doomed to fail from beginning because the lack of convincing evidence.

3. China Medical System can withstand the tests of time, and win the future with its innovative model

China Medical System, which has been operating for the last 25 years as a low-profile company in the Chinese pharmaceutical industry, has long withstood both the tests of time and of the market. As a pharmaceutical enterprise with profound experience, China Medical System also enjoys a special position and irreplaceable value in the pharmaceutical industry chain. It firmly focuses on two core parts of the industrial value chain: product research and evaluation and professional academic promotion.

From the perspective of product R&D model, the R&D innovation of China Medical System differs from the simple self-established R&D or the pure introduction of products for sales. Instead, it effectively integrates two elements and forms the “S+D” (Search & Development) model. This unique “China Medical System Model” not only, to a certain extent, avoids the huge risks and investments of independent R&D, but also ensures its ability in product innovation and control. With its own edge in domestic and overseas resources, this China Medical System R&D model also ensures its strength to compete in the market, thus building a strong core competitiveness.

In just two years, China Medical System has made great achievements in its innovation. It has invested in 7 R&D companies in the United States, the United Kingdom, France and Switzerland; has strategically cooperated with 4 R&D (pharmaceutical) companies in India and Israel; has obtained 19 innovative products in total, 6 of which have been approved for launching overseas, 1 of which is under FDA’s approval process, and 5 of which are in phase III clinical stage, so as to ensure that innovative products can be successively launched into the market in the short-, medium- and long-term. The total annual sales potential of four overseas approved or to be approved innovative products are expected to exceed RMB 10 billion.

The sound historical sales records of China Medical System’s main products and its selling expense ratio which at the low level of the industry, making its professional academic promotion ability obvious to all. Since its listing in 2010, the annual selling expense ratio, excluding the impact of “two-invoice system”, for China Medical System has remained at about 22%. In the context of increasingly strict anti-corruption and compliance control in the industry, the lower-expense-ratio promotion model also reflects the efficiency and compliance of China Medical System’s promotion network. A professional academic promotion network serves as the most suitable foundation for the promotion and development of innovative products, and is also an important weapon for China Medical System to best their competition.

4. Conclusion

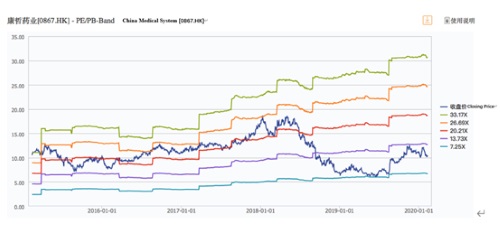

As the Chinese sayings goes, “only the toughest grass can bear strong winds”. From this short selling incident, China Medical System did not suffer from it, but demonstrated a high-quality enterprise who can withstand test to investors. Up to now, many sell-side researchers in the market have also given China Medical System a favorable rating. For example, Phillip Securities Group, in its latest research report, maintained the “overweight” rating with a target price of HK$ 13.35; Credit Suisse raised the target price of China Medical System to HK$ 14.05 at the end of January, and maintained its rating of “outperforming”; Morgan Stanley also gave the target price of HK$ 14.6. In considering of its valuation, the company’s current dynamic PE is about 11 times, at the bottom of the historical range.

The current lower valuation of China Medical System may due to two reasons. Firstly, the market worried about the impact of China’s centralized procurement policy on its existing products, Deanxit and Plendil. However, this policy has been continuously optimized and adjusted, and at present only products with more than two generics consistency passing would be included in the centralized procurement list. According to the inquiry, only one generic of Deanxit has passed the consistency evaluation, while no generics of Plendil have passed this evaluation. Therefore, in the short term, the centralized procurement policy will have no impact on the products of China Medical System. At the same time, the company has also invested in some competitive generics which are supposed to launch to the market as soon as possible, grasping the policy benefit to gain additional revenue. Secondly, the market does not have a comprehensive understanding of the company’s transformation, especially its innovative product pipeline. Currently, the company has four innovative drugs approved or to be approved overseas with great market potential, are in the registration process for China market approval. Once they are approved in China, the innovative product pipeline of China Medical System will be confirmed by the market and bring improvement to the company’s sales performance. Therefore, the current share price of China Medical System still has a large space for restoration.

In retrospect, China Medical System has withstood the long-term tests from time and the market, creating generous returns for shareholders, and also continuing to make contributions to the development of the Chinese pharmaceutical industry. Looking forward, China Medical System will proactively conform the development direction of industry reform with its innovative business model, and continue to strengthen its core values in the entire pharmaceutical industry chain, and enhance its own competitive security margin. It can be concluded that both its current and past excellent performance, along with its long-term core competitiveness, give China Medical System a huge space for imagination in the future.